This is the story of Leodan, the first hybrid private bank. Its story proves that just adding digital to a business really is not the same as creating a digital business. Many incumbent business leaders understand digitization as synonym for making things digital that were done manually before, usually in order to save costs and to increase customer’s self-service capabilities. But automation is just one side of a digital strategy and certainly the lesser one. The other side of digital – less deductive for established businesses but far more powerful – is truly embracing digital and make it part of the DNA. This means to blend it into every aspect of the existing business, to leverage the existing strengths while adding new aspects to them to create something entirely new in the end. I call this the hybrid strategy, an almost universal recipe of how to make “digital” a genuine part of any traditional, relational business.

Once upon a time…

…there was a private bank. It was called PHZ and was founded only in 2009. Yet it was old-fashioned in many ways. The bank was founded by Marcel and Pascal, two long-time private bankers, in the middle of the financial crisis. Their offering was traditional private banking in the very best sense: High quality, personalized wealth management, good service, no excesses, no speculation, no cheating on customers. Although these were also the traditional attributes of private banks, none of them seemed granted anymore. Too many black-money scandals and customer rip-offs, reinforced by the industry’s notorious secrecy, had shaken the private banking industry’s reputation.

So it came that with their clear cut, transparent wealth management approach the bank was actually growing steadily as it did represent a true alternative to the establishment. After 5 years they surpassed 500 million Swiss Francs in assets under management and they were operating profitably, although this asset level was generally considered impossible for a private bank to be profitable with. But ever since inception the bank adhered to one principle that made them profitable now and that also should be the basis for their digital success: Leanness.

The need to change

Despite the early success, Marcel and Pascal along with Victor, the president of the board of directors, felt that this development might not continue if they wouldn’t move on. The world was changing ever more rapidly. Digitization had meanwhile captured most industries and mixed up quite many of them, among them all transactional banking business, such as payments and trading.

However most private banks, and PHZ among them, seemed to remain frozen in the last century with regard to technology. Private banks, along with other traditionally relational businesses, didn’t realize digitization was a trend that was affecting them, too.

Marcel, Pascal and Victor on the other side realized that they needed to do something differently in order to remain competitive in the future. So they did what they always did when they reached out to the unknown: They ran a classified ad in the country’s most respected business newspaper that simply read: “Private bank seeks strategic partners”.

Bringing in technology

At the same time Bruno and Richard, the visionary founders of Crealogix, a respected banking technology company, were foreseeing that the next trend in banking would be digital advisory. And yet they were unable to find a private bank willing to pilot it.

If I’d try to explain the industry’s unwillingness to digitize advisory, one reason could have been that Private Banks considered advisory as their core competence and it was indeed where they created value for customers. They seemed reluctant to digitize their core process as digitization leads also to standardization and hence – they seemed to think – loss of flexibility and service quality. In addition, full digitization would have potentially jeopardized the industry’s goose laying the golden eggs, the so called “discretionary mandates” as robo-advisory technology was managing wealth efficiently and automatically and would make those mandates redundant. It seemed to me a bit like Kodak fearing that digital cameras would make redundant the chemical film business…

The one business case that private banks were seeing however was software-supported human advisory: New regulations such as MIFID (in the EU) and FIDLEG (in Switzerland) were drastically increasing the documentation requirements for client interactions making it virtually impossible to remain compliant with regulations without digital workflows for the advisers. However, this perspective was completely missing the point of digital as a transformational force and enabler for a contemporary customer experience.

Whatever the reasons for the reluctance, Bruno and Richard were disappointed: No matter what private bank they approached, the doors were quickly closed in front of them, as politely ever it was. Private banks just seemed to have other priorities in mind than digital advisory.

So it came that when they read the small ad of the private bank seeking strategic partners they immediately called them up. They sat together and the two companies quickly realized the complimentary nature of their problems, ideas and strengths. Consequently they formed a technology partnership to pilot digital advisory in private banking.

In need of a business model

Some weeks later – the project was already in the process of customizing and building technology – the partners realized that they might have the technology and banking know-how but they were lacking something fundamental nevertheless: A business model to build on. This is when they approached me to support them with that.

When I joined the venture, senior managers from both companies were already deeply absorbed in workshops doing screen designs and detail specifications for risk profiling software. They were in a great hurry and it seemed that they were crystal clear about what they were going for. I admired top management’s personal commitment to the project (though I also was doubtful whether it was a good idea to let senior managers do detail specifications).

Also, despite the detailed level of work being done I felt that there was a lot of ambiguity in the plans nonetheless. To start with I was missing a congruent strategic picture that could have been transformed into a product let alone screen designs. There were bits and pieces around, some of which were even contradictory depending on whom you were asking. I feared that what would come out of the project would be neither fish nor fowl.

There were some agreed goals around such as doing “Private Banking for the smart customer, not for the smart banker” or, what came closest to a vision, the goal of “building a bank for the self-directed customer”. This thinking came straight out of the 1.0-world where there were only two kinds of banks: Traditional players such as private banks for the relational customers and on the other hand the online banks for the self-directed, transactional customer.

Strategy required

Unfortunately, putting self-directed customers at the center didn’t seem to be a good idea to me. This was exactly the clientele that was perfectly well served by the existing banks’ online self-service offering. In addition, self-directed customers were the ones for which the wealth management competence of the private bank could create least value. What those customers needed instead was a good and cheap trading or asset management interface. For the latter, pure robo advisers such as Wealthfront or its Swiss copy-cat TrueWealth were on the rise. They didn’t require (or allow) any human interaction with the wealth manager anymore. Nonetheless the managers were pretty convinced about the self-directed customer target. They were arguing that the competitor bank’s interfaces were technologically (and visually) out-dated so a new player with a contemporary interface would have a competitive edge. They were probably right about the other banks running on outdated technology at the time, but I didn’t buy that a modern interface alone would be a competitive edge.

Consequently, what they were actually specifying in their workshops was a modern e-banking and trading interface with self-advice features for risk-profiling and investment goal setting hidden in an add-on menu.

Putting customers at the center

Instead of building a business model to cater for the self-directed customers right away (what I was hired for initially), I convinced the managers that we needed to take one step back and start by revisiting the value proposition from the customer’s point of view. To do that, we started by reviewing all the customer research available and then based our hypothesis on it.

I’ll cover the methods of how to actually create a value proposition at another occasion. But what came out of the process didn’t surprise me: The “self-direct customer” was gone as target segment. Instead, the insight was rather that the middle grounds were not well covered by any serious offers in the market and were perfectly well suited to be served by the intended mixture of modern technology and wealth management craftsmanship. It simply meant that the managers now assumed – based on the research – that many customers wanted to do their business online, but still appreciated having human beings around for advice and support. It meant that many customers didn’t want to trade all (but maybe some) of their investments by themselves, but neither were they willing to give up control by delegating everything to a bank.

A complex business needs a holistic value proposition

In the end, it was all summed up in the following statement:

We want to become the first bank to serve customers with a new combination of digital and personal interaction. We will take care of client’s wealth in a transparent and efficient way, all while making it possible for them to remain in control and act on themselves whenever and wherever they want, so they can truly be worry-free.

What might sound like a rather general statement was actually giving justice to the complex value proposition of wealth management and it was giving direction to the team. It was also radical for a traditional private bank: Transparency and customer-control were about the arch-enemies of traditional private banking business and yet it felt right to go for it.

Creating the Minimum Viable Product

The pieces all seemed to fall into place now: The value proposition statement was used as a guiding light for all further development. Consequently it became the heart of the Minimum Viable Product for what we now called “the new bank”.

Contrary to the single-dimensioned MVPs of any startup you name, this was the MVP of a new kind of private bank and as such, it contained a total of 16(!) value adding elements supporting the value proposition. In total, we felt that this ensemble would provide exactly the kind of customer experience that was required to solve the intended target audience’s wealth management needs. If you wonder, this is a major difference with regard to Eric Ries’ original lean startup approach: Transforming a relational business usually cannot be done with a single-dimensioned MVP as it wouldn’t add enough value for the customer base nor would it impact employees and business structures enough. The MVP for an established business must touch all relevant aspects of that business, under the sole condition that they are value creating (i.e. solve customer problems better than before). In the case of this private bank the MVP was comprising some (or all) elements of investment strategy, portfolio management, portfolio monitoring, advisory, onboarding, service levels, channels, user interfaces and – it goes almost without saying – branding and marketing.

This MVP was then set in stone to assure that along the way development efforts wouldn’t derive into non-value-adding functionalities. Adding or changing even details of the MVP before going live meant escalating it all up to top management of both the private bank as well as the technology partner.

I’ll give you some examples of how elements were stated in the MVP and how they were transformed into actual features in the end:

Becoming the first hybrid private bank

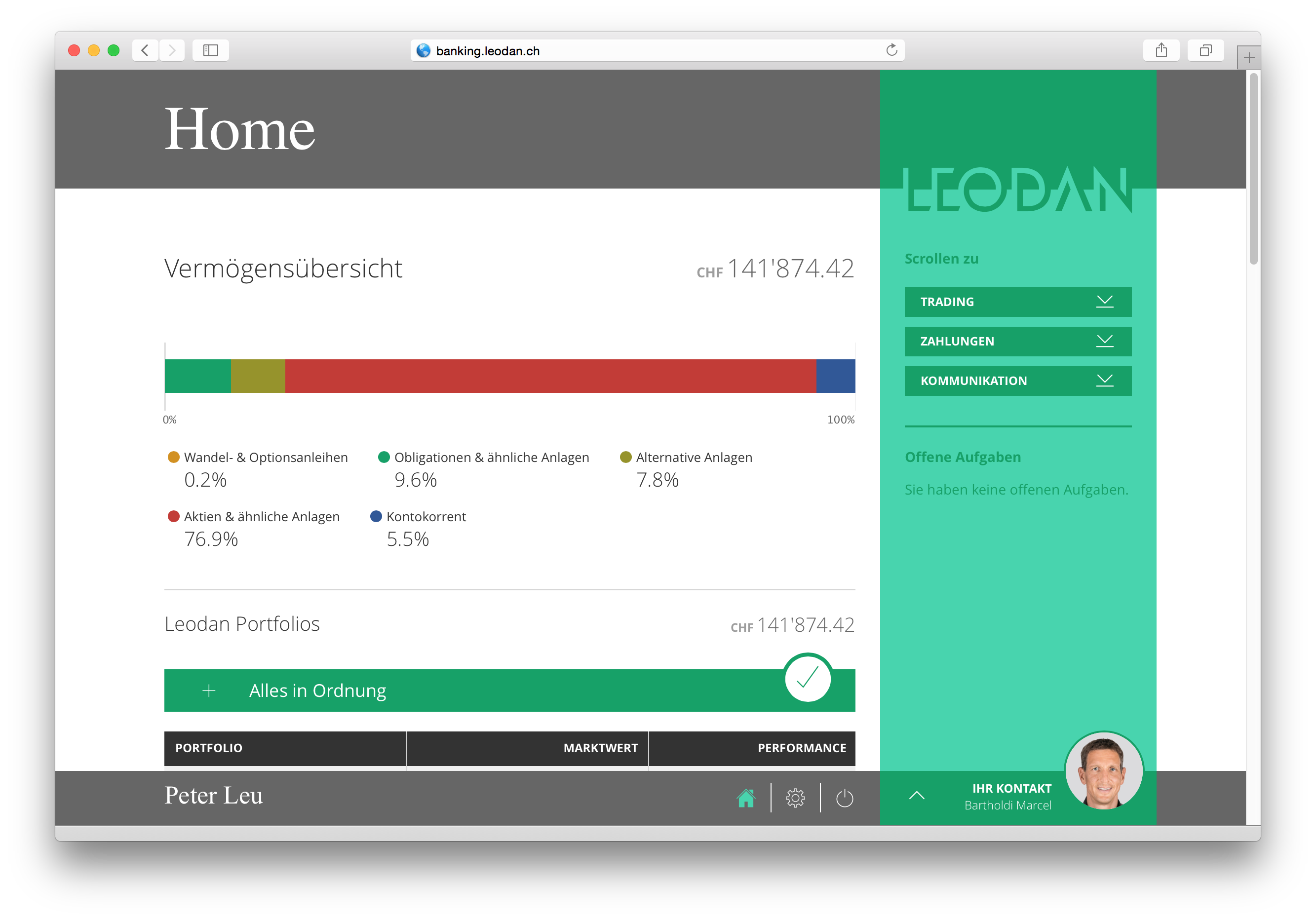

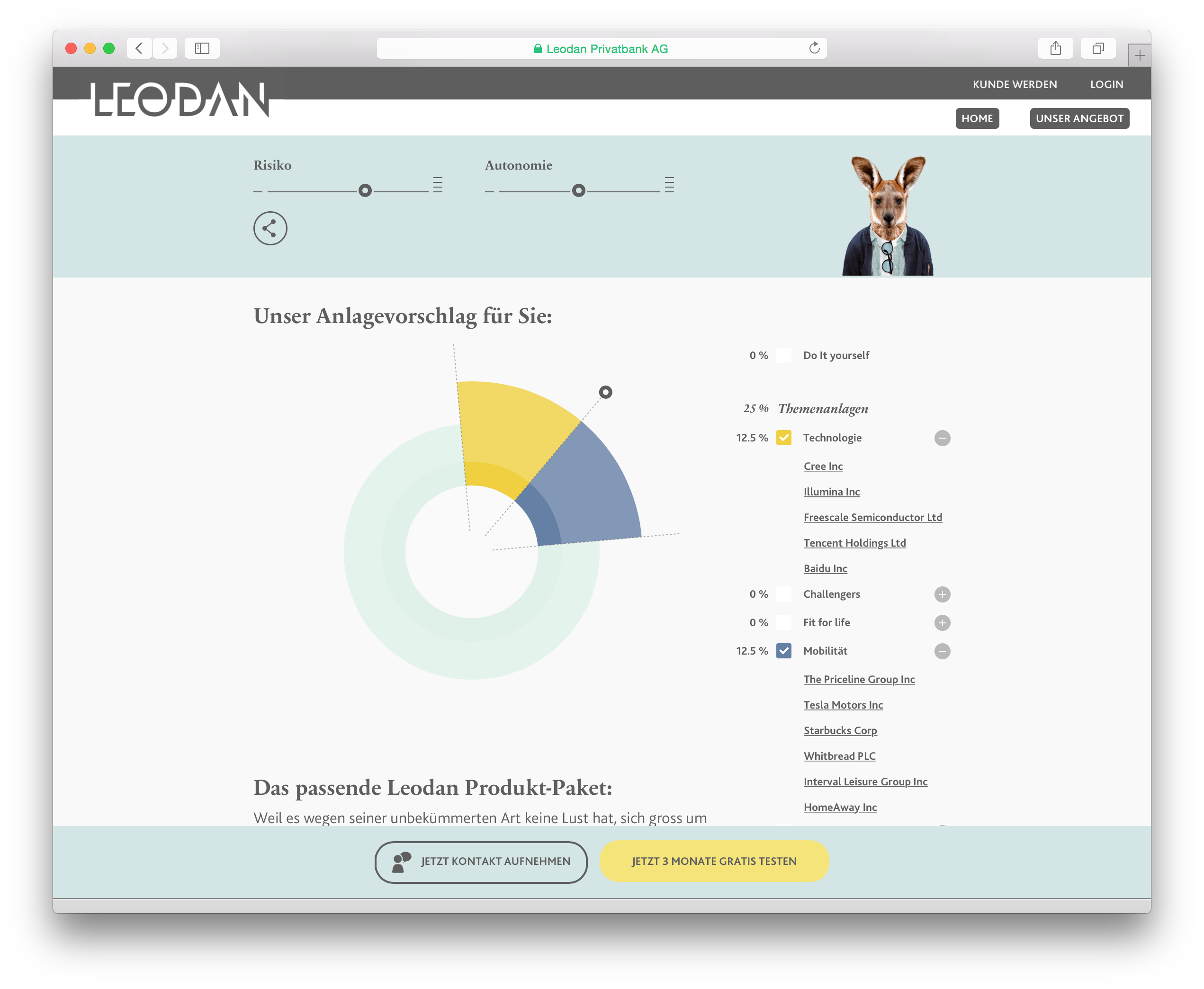

The old private bank was now slowly ceasing to exist as more and more elements blended into the traditional wealth management approach, to rise again as something new, unique and exciting: A private bank like no one before. It has become clear now that we couldn’t drag along the old legacy but also had to gain an entirely new identity. Leodan® took shape, blending inherent characteristics of both traditional private banks as well as modern Internet banks. It would manage wealth for customers just as it would let them trade all on their own, or anything in between.

The term that appealed to the bank for this idea of blending things together was “hybrid”, which was later coined as Hybrid Private Banking® into an integral part of the branding:

![]()

Once the target value proposition was clear, the path ahead became clear as well: Deriving the business model for instance was now the literal walk in the park. I’ll cover how to do that at another occasion as well. However, it would still be a long journey of almost two years to bring the new bank to life. A journey on which besides the business model, values, brand identity, naming, design, positioning, reason why, offering, pricing, investment strategy, product, marketing, sales, HR strategy and many other things needed to be revisited and defined. This journey was just about to begin.

Epilogue

The hybrid value proposition is much more than only Leodan’s unique strategy and identity statement. It’s actually a universal strategy recipe of how to make digital a genuine part of any traditional, relational business: It means not to give up any of your strengths but on the contrary to become aware of them, focus on them and then enrich them with the power of digital technology. But in order to do so, you will need the willingness and courage to truly transform your business into something new that will rise from this process, just as Leodan did.

Learnings from the Leodan case:

- Don’t do what is convenient: do what is right

- Be committed to change your DNA, although it’s going to hurt

- Put customer’s at the center of your reflections, without compromises

- Put technology and business know-how at eye’s height

- Design a value proposition that embraces what is value creating in your business already as well as what is adding value from new digital features

- Stubbornly fixate on the MVP until it’s live

- Design a business system, that will remain flexible in the future

> Read about the hybrid strategy

Follow me:Share this page: